{kind=link}

The $3.2 billion includes an estimated $150 million in transaction-related taxes owed by the acquired entities, and is otherwise structured as 70% cash and 30% Cadence common stock. Devgan expects the deal to add an additional $160 million in revenue to Cadence by 2026, based on the company’s financial model.

Five compelling reasons for Cadence to buy Hexagon D&E division

Here are the key reasons for the acquisition:

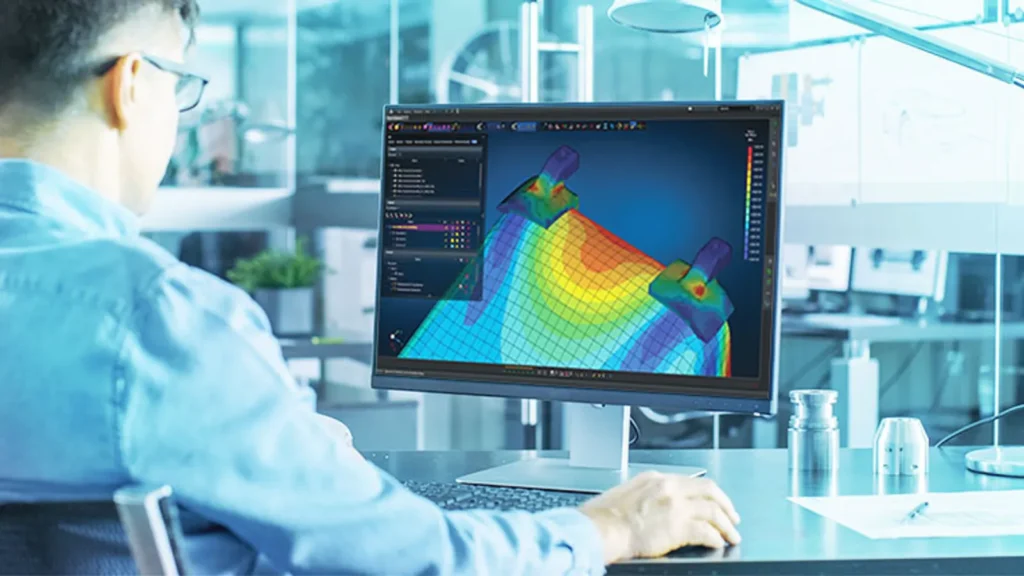

• Expanded multiphysics capabilities: The acquisition brings world-class simulation tools such as MSC Nastran (structural analysis) and Adams (multibody dynamics) to the Cadence fold. This complements Cadence’s existing capabilities in computational fluid dynamics (CFD) and its recent acquisition of BETA CAE, creating a comprehensive platform covering structures, motion, electromagnetics, fluids, and thermal analysis.

• Driving “intelligent system design” and physical AI: The deal bridges the gap between electronic design (chips) and mechanical design (physical systems). By coupling high-quality, physics-based simulation with AI-driven design, Cadence aims to accelerate the development of “physical AI,” which is critical for autonomous vehicles, robotics, and complex, intelligent systems.

• Expansion into key industries: Hexagon D&E has a strong, established presence with leading aerospace and automotive OEMs and Tier 1 suppliers (e.g., Volkswagen Group, BMW, Toyota, Boeing, Lockheed Martin). This will enable Cadence to deepen its market presence in these critical sectors as they transition to electric vehicles and autonomous driving.

• Strategic shift to “system-level” design: As electronic and mechanical components become more integrated (e.g., in advanced chiplet packaging), the demand for simulation tools that can analyze entire systems rather than just individual components has increased. This acquisition positions Cadence as a leader in this converging market.

• Financial and growth synergy: The D&E business generates strong, recurring revenues, with approximately €265 million generated in 2024 and an expected positive impact on Cadence’s revenues in 2026. It brings over 1,100 employees with deep expertise in simulation.

Siemens Digital Industries has a “holistic edge”

In general, notably the EDA industry segment is currently dominated by the “big three” (Synopsys, Siemens EDA, and Cadence). Together, they control ~90% of the market and are aggressively building internal capabilities and engaging in strategic mergers and acquisitions to strengthen this “systems-to-silicon” strategy.

A generally interesting observation from a holistic perspective, including both product development and production technology, is that Siemens, by virtue of its domain-wide and deeply integrated Xcelerator portfolio and its smart factory knowledge, has a head start across the entire value chain.

This holistic angle of attack is growing in importance as users develop increasingly complex products. Technologies that enable collaborative design of mechanical, electrical, and software systems are growing rapidly, among other things because they contribute to faster time to market.

The PLM market experienced significant growth in 2024 (2025 figures from analyst CIMdata will be available in mid-2026), with particular strength in the EDA and AEC tools segments, driven by increasing demand for electronics and the digitization of even the oldest infrastructure to benefit from digital twin implementations. ‘Focused Applications’ (ALM) continue to outperform core solutions for comprehensive collaborative product definition management (cPDm) as the richness of PLM ecosystems broadens, and system integrators increasingly see increased demand for their service offerings.”

Among the sub-PLM areas, EDA tools (Electronic Design Automation) still hold the position as the largest segment by far, with a total of $19.3 billion in investments and also with an increased share of the total from 23% in 2023 to 24% in 2024. Second on the sub-PLM side in 2024 was, as in 2023, cPDm with $11 billion invested and a share of the total of 13.7%, closely followed by third place Simulation & Analysis, with $10.9 billion invested and a share of 13.6%.